By Larry Stalcup Contributing Editor

Early data from the U.S. Department of Agriculture’s (USDA) new Cattle Contracts Library (CCL) pilot program solidifies the notion that higher quality cattle bring higher prices. And with the magnitude of information on overall packer specifications and pricing, it’s up to producers and feeders to read how better genetics and production methods can improve their profits.

The Agricultural Marketing Service (AMS) started the CCL program in January. The pilot continues through Sept. 30, 2023. Its goal is to increase market transparency and price discovery. It requires packers that harvest 5 percent or more of the overall national slaughter (basically the four major packers) to provide contract information for the purchase of cattle, as well as the number of actual and estimated cattle purchases under active contracts.

The majors – JBS, Cargill, Tyson and National – are required to provide detailed data over and above what they already provide to USDA and other sources. In reviewing the March 3 report, CCL’s January contracts totaled 1,004,631. The report estimated that February contracts totaled 989,796.

Of those February contracts, about 764,000 were from USDA reports; about 137,000 were from negotiated contracts; about 82,000 were from top-of-the-market reports and about 22,000 were from CME delivery cattle.

The USDA report showed:

- 35.17 percent were based on Nebraska’s weekly slaughter.

- 34.22 percent were based on Kansas weekly slaughter.

- 23.73 percent were based on Texas-Oklahoma weekly slaughter.

- 5.08 percent were based on the five-area weekly weighted slaughter (Texas/Oklahoma/New Mexico; Kansas; Nebraska; Colorado; Iowa/Minnesota).

- 1.27 percent were based on Iowa/Minnesota weighted average cattle report.

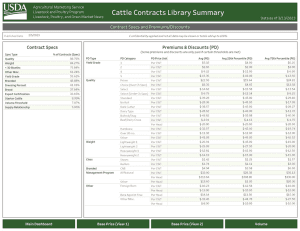

Contract specs used in the program show that USDA Quality Grade (86.76 percent) and weight (84.27 percent) were the highest considerations in the contracts (see Figure 1). For cattle under 30 months of age, USDA Yield Grade, branded programs and breed were also major considerations in contract specs.

Premiums and Discounts

Likely the most telling CCL data (see Figure 1) show the value of quality cattle in the selling price. Fed cattle that graded Prime had a price that showed an average premium of $22.95 per cwt. Prime carcasses in the 25 percent level averaged $19.64, while those in upper 75 percent or higher hit $24.81.

Carcasses that graded high Choice showed an average premium of $8.35 per cwt. Premiums ranged from $4.65 in the lower 25 percent to $13.58 for those 75 percent or higher. Yield Grade 1s and 2s also produced slight premiums. All-Natural cattle showed an overall premium of $32 per cwt.

The big hit comes with discounts seen for Select grade carcasses. The average discount was -$14.62 per cwt., with discounts ranging from -$15.58 for the lower 25 percent and -$13.54 for the upper 75 percent. No Roll, Standard and Dark Cutter carcasses had discounts ranging from about -$28 to -$39 per cwt.

Beef/dairy-cross carcasses showed there was only about a -$3 per cwt. discount. However, straighter dairy carcasses had an average discount of about -$28 per cwt.

Glynn Tonsor, Kansas State University Extension livestock marketing economist, points out keys in the premium breakdown that producers can benefit from. “The 25 and 75 percentile detail can provide users guidance on the distribution of premiums and discounts in the market,” he says.

“For instance, consider the last report [March 3] and All Natural. The $32 per cwt. average value is augmented by $28.38 [25th percentile] and $35.13 [75th percentile]. This indicates only 25 percent are getting over $35.13 per cwt., suggesting premiums much above that may be hard to obtain.

“The available premium/discount information can give insight into marginal increases in revenue, which can be compared to the costs of paying more to buy an animal and/or raise it in a way that complies with a said claim.”

Brady Miller, Texas Cattle Feeders Association (TCFA) marketing director, says the value of using CCL to monitor quality depends on a producer’s decision to either retain ownership of the cattle or to sell the cattle off the ranch.

“If producers decide to sell their cattle to a feedyard and don’t know the quality of the animals being produced, then the only advantage of knowing this information would be to better understand the value of producing a premium animal and the added value that is potentially being left on the table,” Miller says.

“For producers who retain ownership of their calf crop, the CCL reports show the highs and lows on premiums and discounts and what can be expected if cattle fall within some of the different programs,” he continues. “Higher quality cattle marketed through an alternative marketing agreement are rewarded with more premiums and fewer discounts, which starts with good genetics.”

Elements of the CCL have been published since Livestock Mandatory Reporting was developed 20-plus years ago. “In the CCL, USDA has packaged the information in a different format that allows us to look into the future to see what the contracts are,” Miller says. “It shows us the number of cattle being traded by using these parameters.

“The other piece of the puzzle that we haven’t seen before is how the base prices are determined for cattle sold through alternative marketing agreements,” he says. “Knowing more information about how base prices are determined, premiums, discounts and spreads, might provide incentives for producers to enhance their genetics or change their production practices. There may also be opportunities for producers to negotiate a better deal by considering other marketing arrangements.”

Who Benefits the Most, Packers or Producers?

Some question whether CCL data will benefit packers more than producers and feeders. “Time will tell,” Miller says. “Since USDA only requires the four major packers to report data into the CCL, there are concerns that packers can decipher the data in a much more in-depth and expeditious manner than cattle producers and cattle feeders. It’s a lot of data, and it takes analysts to review, interpret and draw conclusions from it.”

TCFA contends the CCL should also use data from smaller packers and those scheduled to come online. “USDA would say we are seeing 85 percent of the contracts by limiting the CCL to the majors, but it would be helpful to have a more comprehensive library that includes other companies and packing plants,” Miller says.

“If we as an industry want a true picture of all contracts, then it’s important to see contracts from the regionals and from the new packers coming online in the next few years. This would help expand participation in the CCL from 18 plants it encompasses today to about 40 plants,” he says.

“It would make it more difficult for the major packers to blackout their own data and ‘see’ what their competitors are doing.”

Additional contract information has the prospect of assisting cattle buyers and sellers make better guided decisions, Tonsor adds, but “exactly how much these AMS reports increase information for both sides is debatable.”

For instance, since only about 2 percent use the Iowa reported price as a contract’s base, “it illustrates how said reports can illuminate new information to some parties and not necessarily all parties in the industry,” Tonsor contends.

“On balance, I do not expect CCL to be a game changer. If it can be administered in a way that is not too costly while providing useful information and protecting the confidentiality of buyers and sellers, then it can be beneficial in some aspects.”